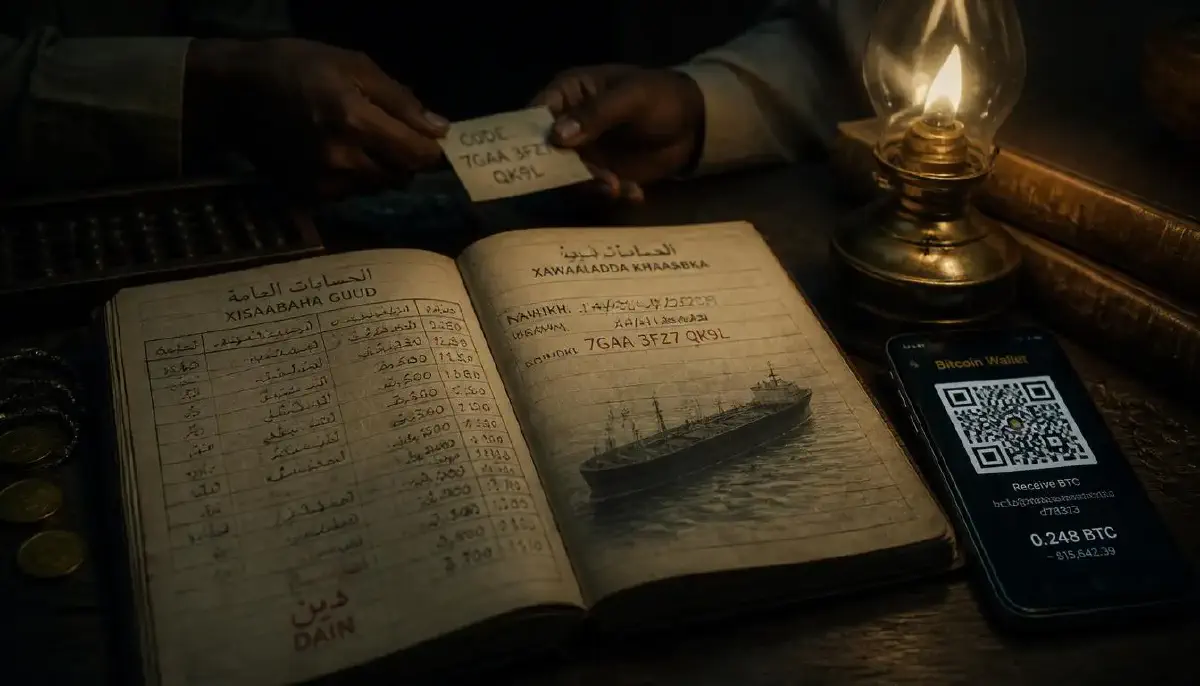

In a cramped office above a market in Mogadishu, a man we will call Abdi sits behind a desk cluttered with mobile phones, ledger books, and a single laptop. He is a hawaladar—a broker in the ancient trust-based money transfer system known as hawala. On a typical morning, he receives instructions by text message or WhatsApp from Somalis in London, Minneapolis or Dubai: send $200 to a family in Baidoa, $500 to a cousin in Hargeisa, $1,000 to a business partner in Nairobi. He notes each transaction in a leather-bound notebook. By the end of the day, his office has moved tens of thousands of dollars across borders and time zones. No money has physically travelled. No bank has been involved. No regulator has been informed.

Abdi’s work is not a reversion to pre-modern finance but a sophisticated adaptation to its collapse. Somalia has been without a functioning central banking system since the state disintegrated in 1991. Formal financial institutions are scarce—fewer than 9% of Somali adults have a bank account. Yet the country receives an estimated $2 billion in diaspora remittances each year, a sum that sustains more than half of all households and accounts for between 17% and 23% of GDP. The vast majority of these funds—over 55%—arrive through hawala. Mobile money handles most of the remainder. The formal banking system is almost entirely irrelevant.

This pattern is not unique to Somalia. Across the world’s conflict zones, from Yemen to Syria, from Afghanistan to the Sahel, the regulated financial system has either atrophied or been deliberately severed—by sanctions, by blockades, by the destruction of physical infrastructure. Into the void steps a constellation of informal networks: cash couriers, commodity smugglers, crypto exchanges, shell companies, and ghost fleets. Together, they form the shadow ledger of war—an invisible balance sheet that operates in parallel to the official one, and that is every bit as consequential for who wins, who loses, and who profits.

The hawala advantage#

Hawala operates on a principle of extreme simplicity. A sender in, say, London gives money to a hawaladar there, along with a code. The London hawaladar contacts a counterpart in Mogadishu, who dispenses the equivalent amount in local currency to the recipient who presents the matching code. The two hawaladars settle their balances later through trade invoices, commodity shipments, or reciprocal transfers. No money crosses the border. The entire system runs on reputation, familial ties, and the brutal enforcement mechanism of communal ostracism for any broker who fails to honour a commitment.

The advantages in a war zone are obvious. Hawala leaves no digital footprint that can be traced by an adversary or frozen by a sanctions regime. It can operate without electricity or internet—though it now uses both to increase speed. It reaches villages that have never seen a bank branch. And it is, by the standards of the formal banking system, remarkably cheap: fees are typically a flat percentage, embedded in the exchange rate, and far lower than the 10–20% that Western Union might charge for a corridor deemed high-risk.

The West has viewed hawala with suspicion since the attacks of September 11th 2001, when it was revealed that some of the hijackers had received funds through informal channels. Regulation has tightened, and the major hawala networks have been compelled to register as money-service businesses and implement anti-money-laundering controls. But in practice, the system remains largely opaque. In Afghanistan, where the Taliban’s takeover in 2021 severed the country from the global banking system, hawala is once again the primary conduit for aid payments, remittances, and the illicit opium trade that funds the regime. In Syria, hawala networks route money between the regime-held west and the rebel-controlled north, financing everything from food purchases to weapons smuggling.

The humanitarian community has learned to live with this reality. UN agencies and NGOs routinely use hawala to pay local staff in areas where banks are closed or transactions are monitored. The alternative—shipping cash in suitcases or armoured vehicles—is more dangerous and more expensive. Hawala, for all its risks, is simply too useful to be abandoned. The shadow ledger is not a rival to the formal system; it is the only system left standing.

The crypto front#

If hawala is the ancient art of informal finance, cryptocurrency is its digital heir—and it has found a natural home on the battlefields of the 21st century. The war in Ukraine was the first major conflict in which crypto played a visible, publicly documented role, and the results were striking.

In the first days of the invasion, the Ukrainian government posted Bitcoin and Ethereum wallet addresses on its official Twitter account. Within a week, it had received over $50 million in crypto donations from around the world. By early 2025, the total had climbed to roughly $200 million, including $80 million in direct government donations and the rest funnelled through a network of DAOs (decentralised autonomous organisations) and NFT sales. Ukraine’s crypto advantage over Russia in fundraising was at one point estimated at 44 to 1. The funds were used to buy drones, body armour, medical supplies, and—in a particularly meta application—to develop software for digital warfare.

Russia, for its part, has used crypto more for sanctions evasion than for crowdfunding. Pro-Kremlin paramilitary groups, including the notorious Rusich unit, solicited donations in Bitcoin and even charged families for the coordinates of their fallen relatives’ bodies, payable in cryptocurrency. Russian-language darknet markets have facilitated the purchase of dual-use technologies, from microchips to thermal imaging scopes, using crypto as the settlement layer. The total volume of Russian crypto fundraising—roughly $5 million by early 2025—pales in comparison to Ukraine’s, but it is almost certainly an undercount of the true scale of crypto-enabled sanctions evasion.

The emergence of crypto as a tool of war finance has provoked a regulatory scramble. The blockchain forensics firms that trace these flows—Chainalysis, Elliptic, TRM Labs—have become the new intelligence analysts of the financial battlefield, identifying wallets, tracking transactions, and providing evidence for sanctions designations. Yet for every wallet that is frozen, a dozen more are created. The technology is inherently borderless, and the developers who build it have shown little interest in policing its use. The result is a financial environment in which the combatants, not the regulators, hold the initiative.

The ghost fleet#

The most visible manifestation of the shadow ledger sails the world’s oceans. Russia’s “ghost fleet” of oil tankers—vessels that operate with opaque ownership, doctored transponders, and no meaningful Western insurance—has become the centrepiece of the Kremlin’s sanctions-evasion strategy. The fleet, by mid-2024, numbered more than 400 crude-oil carriers and roughly 200 product tankers, accounting for about a fifth of the global crude tanker fleet and over 60% of Russia’s seaborne oil exports. In 2024, these ships moved oil worth more than €80 billion.

The mechanics are well documented. A Russian crude-oil tanker loads at a Black Sea or Baltic port, often under the flag of a non-aligned state such as Gabon or the Cook Islands. The ship’s Automatic Identification System transponder is switched off or manipulated to hide the vessel’s true movements—a practice known as “going dark.” Mid-ocean, the oil is transferred to another tanker in a ship-to-ship operation that is difficult for satellites to monitor in real time. The receiving vessel carries freshly doctored bills of lading that obscure the oil’s Russian origin, and it sails to a refinery in India, China or the Middle East, where the product is blended, refined and re-exported. By the time it reaches a Western consumer, its provenance is laundered beyond recognition.

More than 90% of these ships sail without proper Western insurance, relying instead on a patchwork of Russian state-backed cover and unrated insurers in jurisdictions with minimal regulatory oversight. The environmental risk is enormous: a major oil spill from an uninsured, poorly maintained tanker would create a disaster whose liability would be almost impossible to assign or recover. In the narrow chokepoint of the Strait of Hormuz, where a significant fraction of the world’s oil transits and where naval mines and drone attacks have become a feature of the Iran-Israel proxy conflict, the convergence of ghost fleets, wartime hazards, and marine biodiversity creates an ecological time bomb that no one seems willing to defuse.

The gold smugglers' route#

Not all shadow flows are electronic. In the conflict zones of central Africa, gold smuggling provides a direct link between the battlefield and the global bullion market. Artisanal mines in the eastern Democratic Republic of Congo, South Sudan and the Central African Republic are controlled by armed groups who use the proceeds to buy weapons, pay fighters, and finance their operations. The gold is smuggled overland to Uganda, Rwanda and the United Arab Emirates, where it enters the legitimate supply chain—a process facilitated by lax regulation in Dubai’s gold refineries and the near-impossibility of tracing the origin of a melted gold bar.

The United Nations Group of Experts on the DRC has documented this trade in painstaking detail. In 2023, it estimated that over 95% of the gold exported from the eastern DRC was being smuggled. The annual value ran to hundreds of millions of dollars—a figure that, if captured by the state and invested in development, would transform one of the world’s poorest countries. Instead, it funds a perpetual war economy, in which violence is not a temporary disruption but a permanent business model.

The regulators' dilemma#

The shadow ledger poses a dilemma that no one has yet resolved. On the one hand, the informal networks that keep money moving in war zones are also the networks that keep people alive. Hawala delivers remittances to starving families. Crypto wallets enable dissidents and refugees to preserve their savings when the banking system collapses. Gold smuggling provides a livelihood for millions of artisanal miners who have no other source of income. To shut these channels down entirely would cause immense human suffering.

On the other hand, the same channels fund terrorism, sanctions evasion, and the prolongation of conflicts. They undermine the effectiveness of economic sanctions, which have become the West’s weapon of choice in an era when direct military intervention is politically unpalatable. They create zones of impunity in which warlords, oligarchs, and paramilitary groups can operate without fear of financial consequences.

The response, to date, has been piecemeal. The Financial Action Task Force (FATF) has tightened its standards for money-service businesses and virtual-asset service providers. The European Union has imposed sanctions on specific hawaladars and crypto exchanges linked to terrorist financing. The maritime insurance industry has developed new tools to identify and refuse cover for vessels that engage in deceptive shipping practices. But none of these measures has succeeded in closing the gap between the formal and the shadow ledger. As long as there is a demand for informal finance—and as long as the formal financial system remains inaccessible or hostile to those living in conflict zones—the shadow ledger will thrive.

In the end, the shadow ledger is not a bug in the architecture of war finance. It is a feature. It is the mechanism by which capital adapts to the destruction of its normal channels, and it is as resilient as the cockroach after the nuclear blast. The challenge, for the regulators and the prosecutors, is not to eliminate it—that is impossible—but to ensure that its benefits flow more to the victims of war than to its perpetrators. The balance of payments of a war zone is rarely settled in a bank. More often, it is settled in a notebook, a blockchain, or the hold of an aging tanker, somewhere on the horizon, where the lights have been switched off.

This is the fourth article in a six-part series, “The Balance Sheet of Battle.” The next instalment will explore the insurers of apocalypse: the war-risk underwriters who price the probability of a missile strike, and who quietly shape the economics of modern warfare.