For half a century, a financial arrangement forged at the end of the French empire has operated largely out of sight, quietly channeling value from 14 African states back to Paris. While colonial flags were lowered, a system of monetary rules, resource contracts, banking practices, and military guarantees was erected in their place. The results can now be measured: between 1980 and 2018, sub-Saharan Africa received nearly $2 trillion in foreign direct investment and official development assistance—and simultaneously emitted over $1.3 trillion in illicit financial outflows, leaving a net negative balance that challenges any narrative of benevolent partnership.

Four interlocking components form this self-reinforcing machine. Altering any one of them—currency, resources, banking, or security—has historically triggered counter-pressures from the others, restoring the equilibrium. Understanding the mechanics requires examining each in turn, beginning with the most visible symbol of the arrangement.

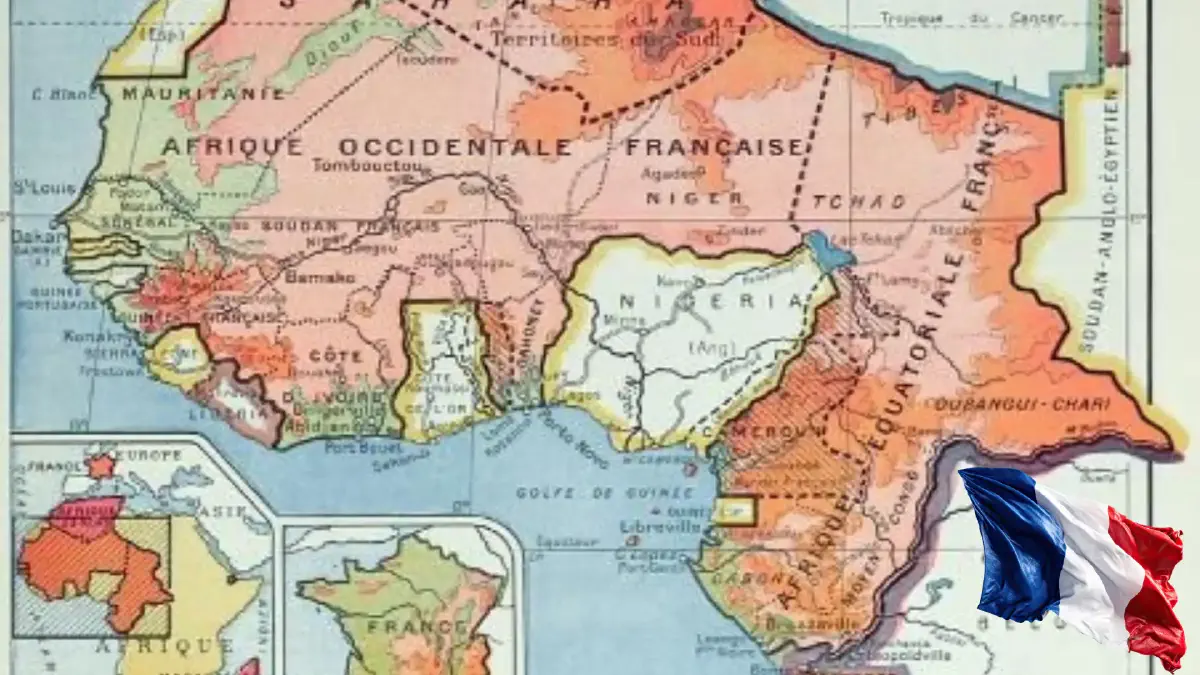

I. The Monetary Straitjacket: The CFA Franc#

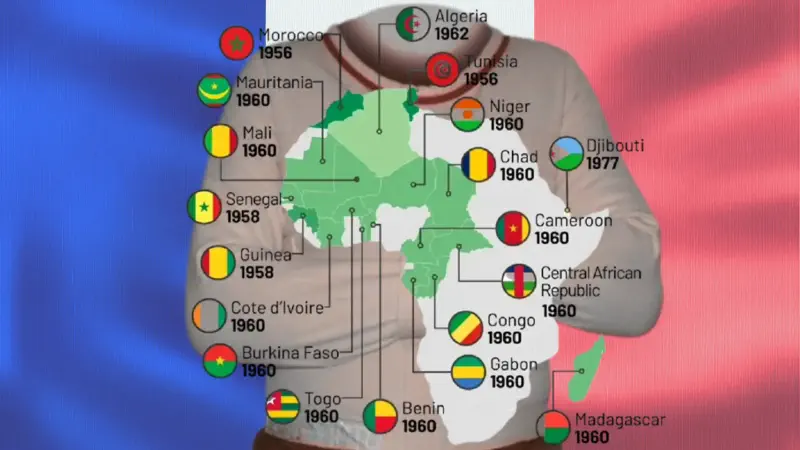

The CFA franc is not merely a currency. It is a mechanism. Born in 1945 as the "franc of the French colonies in Africa," the name was changed to "African Financial Community" after independence, but the architecture remained intact. Fourteen countries across West and Central Africa use it, their money pegged to the euro at a fixed rate of 655.957 CFA francs to €1.

The most contested feature was the "operations account." Member states were required to deposit 50% of their foreign exchange reserves with the French Treasury.In 2023, the Central African central bank, BEAC, received 196.7 billion CFA francs in interest on those deposits—a 358% increase from the previous year.Supporters framed this as the price of convertibility: France guaranteed the peg, and the reserves served as collateral. Critics saw a different transaction—French access to cheap, pooled foreign exchange, while African central banks lost control over a core instrument of monetary sovereignty.

The feedback loop was self-stabilising. Pegged to a strong currency, CFA economies could not use devaluation to regain competitiveness. When the French government unilaterally imposed a 50% devaluation of the CFA franc in 1994, it demonstrated where authority ultimately resided.The 2019 reform that ended the reserve requirement for West African states was hailed as a break with the past.Yet the Central African bloc was left untouched, and the peg to the euro remained.Critics noted that France had already "jumped the gun" by renaming the West African CFA franc to the "Eco," pre-empting a broader ECOWAS currency project and angering several regional leaders.A genuine single currency for West Africa has been repeatedly deferred—now targeted for 2027.

Morten Jerven's research on African statistics adds a further caution. When GDP data are unreliable, as he demonstrates in Poor Numbers, a currency peg based on those numbers becomes an exercise in navigating without instruments.The stability the CFA franc provides may therefore be stability of a particular kind: predictability for French firms repatriating profits, at the expense of genuine monetary flexibility for the states that use it.

II. Unequal Markets: The Resource Rent Machine#

The second component operates through contract rather than currency. French companies enjoy a dominant position in key sectors across former colonies, particularly in extractive industries, where the terms of engagement have historically been set in Paris boardrooms rather than African finance ministries.

Niger's uranium industry illustrates the asymmetry. For over 50 years, the French state-owned company Orano (formerly Areva) has mined uranium around Arlit. The operation has extracted over 145,000 tons, with another 174,000 tons identified at a nearby deposit. At October 2024 uranium prices, the total known resource—319,000 tons—was worth approximately $53.27 billion.Meanwhile, Orano reported global revenues of €5.87 billion in 2024, up 23% from the previous year.Niger's military government, which seized the Somair mine in December 2024, claimed that Orano had appropriated 86.3% of total production value between 1971 and 2024, leaving Niger with a small fraction of the wealth extracted from its soil.

The pattern recurs across sectors and borders. In Senegal, the French mining company Eramet, through its subsidiary GCO, generated over 1,106 billion CFA francs in revenue, but the Senegalese state received only 51 billion CFA francs in royalties—4.64% of the total. Tax avoidance by mining multinationals in sub-Saharan Africa is estimated to cost governments up to $730 million annually in lost revenue.Beyond extraction, the relationship extends to banking and telecoms, where French groups—BNP Paribas, Société Générale, Orange—control critical infrastructure and financial flows across the francophone region.

This component reinforces the monetary one. When resource revenues are systematically under-priced and under-taxed, the state's fiscal base narrows. A narrow fiscal base makes it harder to accumulate the reserves needed to leave a currency union. The peg, in turn, makes it harder to capture resource rents through exchange-rate adjustments. Each mechanism strengthens the other.

III. The Drainage of Wealth: Illicit Flows and Legal Avoidance#

If the monetary union is the plumbing and resource extraction the pump, the third component is the leak in the pipe. Capital flight from Africa—through trade misinvoicing, abusive transfer pricing, and outright corruption—has been documented at a staggering scale.

The Global Financial Integrity programme estimates that sub-Saharan Africa lost over $1.3 trillion in illicit financial flows between 1980 and 2018, an amount roughly equal to the combined GDP of the region in a single year. UNCTAD's 2025 report estimates the annual cost at $88.6 billion. A 2022 study estimated trade misinvoicing in sub-Saharan Africa alone at $152.9 billion for that year.

The mechanisms are well-documented but difficult to prosecute. A French multinational operating in Niger, for instance, contributed 30% of the company's uranium requirements but received only 7% of the payments—a pattern consistent with profit shifting through intra-company pricing. Tax and royalty payments were estimated to be €11-30 million less than they should have been in 2015, equivalent to 8-18% of Niger's entire health budget.

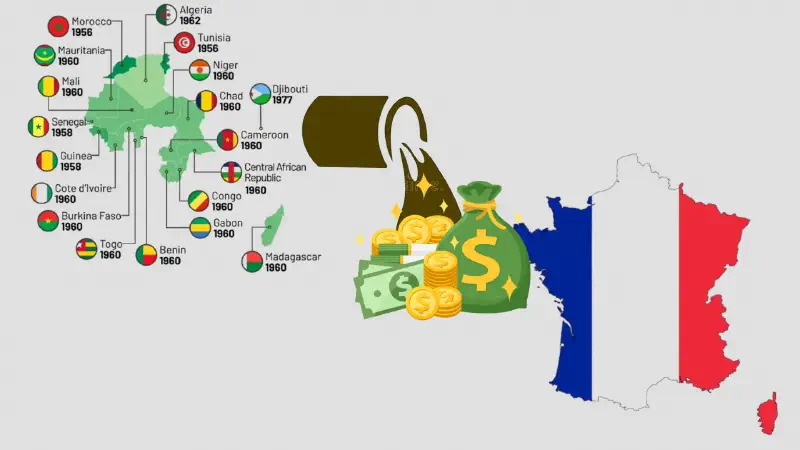

The counter-intuitive result is that Africa has functioned, in net terms, as a creditor to the rest of the world. The outflows systematically exceed the inflows—aid, investment, and remittances combined. France's official development assistance to sub-Saharan Africa, which stood at $4.85 billion in 2022, must be set against these larger currents. In 2025, the French Development Agency's Africa budget was cut by one-third, from €6 billion to €4 billion. At the same time, French foreign direct investment in Africa rose to an estimated €60-68 billion. The state appears to be withdrawing while private capital advances—a pattern that shifts risk onto African governments while concentrating returns in French corporate balance sheets.

IV. The Enforcer: Military Presence as a Backstop#

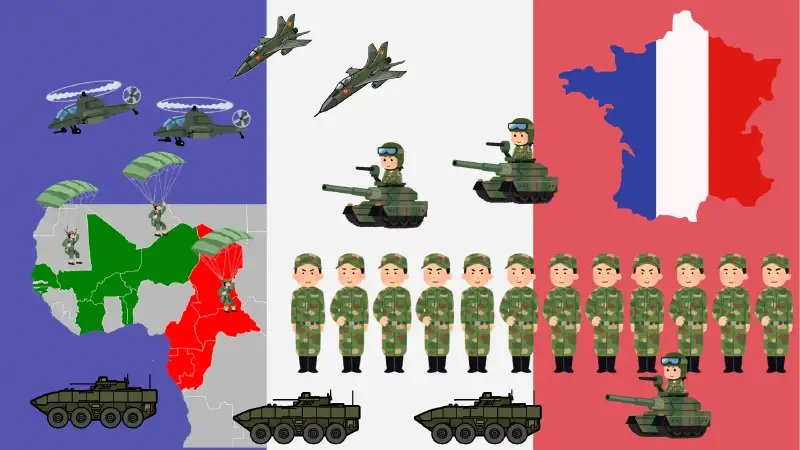

The fourth component is the least visible in economic data but arguably the most consequential in maintaining the system. French military bases and intervention forces have provided a security guarantee—not just for African regimes, but for the economic architecture itself.

A 2008 defense agreement between France and its former colonies, declassified years later, revealed that France maintained pre-positioned forces and intervention rights as part of its strategic posture. In practice, French troops have intervened repeatedly: in Côte d'Ivoire (2002, 2011), Chad (multiple occasions), Mali (2013), and the Central African Republic (2013). Each intervention was justified on humanitarian or counter-terrorism grounds. But each also occurred in states that were economically or strategically significant to French interests—whether uranium in Niger, oil in Chad, or regional stability in Côte d'Ivoire.

The feedback loop operates as follows: political instability threatens the commercial and monetary arrangements described above; French forces restore order; the restored order enables continued extraction and currency stability; the extraction generates the economic surplus that makes French military presence strategically worthwhile. Breaking the loop at any single point has proven difficult precisely because the other three components compensate.

The Sahel coups of 2022-2024 tested this architecture directly. Mali expelled French troops in 2022, ending a nine-year operation. Burkina Faso followed in early 2023. Niger, after the July 2023 coup, demanded the withdrawal of 1,500 French forces by the end of the year. In each case, the new military governments also signalled their intention to reconsider the monetary and resource arrangements—a simultaneous assault on multiple components that the system had never before confronted at once.

The strategic pivot has been swift but uncertain. The Alliance of Sahel States (AES)—Mali, Burkina Faso, and Niger—has deepened ties with Russia, including security cooperation. Central African Republic adopted Bitcoin as legal tender in 2022 and launched a "Sango" project to tokenize natural resources.Sudan has experimented with gold-backed digital currency. These experiments, while still nascent, represent the first systematic attempt in decades to build alternative financial and security architectures that bypass all four components of the Françafrique system simultaneously.

The System Confronts Its Limits#

The resilience of a self-reinforcing system lies in its interconnectedness—and so does its vulnerability. When pressure is applied to a single component, the others absorb the shock. But simultaneous pressure on all four—monetary, commercial, financial, and military—creates a different kind of crisis.

In 2025, the African Union declared the Year of "Justice for Africans and People of African Descent Through Reparations," explicitly targeting the legacy of colonialism and neocolonial structures.The Algiers Declaration, adopted later that year, called for the recognition of colonialism as a crime against humanity and the creation of a permanent reparations mechanism.France ratified the law ending its formal role in the West African CFA franc in late 2025.But the Central African CFA franc remained unreformed, and the ECOWAS-wide Eco currency—the genuine monetary decolonisation that regional leaders have sought for two decades—remained a negotiating position rather than an accomplished fact.

Whether the four-part system is being dismantled or merely reconfigured is the central question for the decade ahead. What the data demonstrate is that the extraction was real, measurable, and sustained. What the current ruptures reveal is that the system depended, ultimately, on consent—and consent, once withdrawn across an entire region, cannot be restored by financial inducement or military force alone.

Infographic#

This infographic gives an overview of the series

References#

Here is a numbered list of the sources referenced in the article, formatted in APA style (7th edition). Wherever possible, I have provided complete bibliographic details; in a few cases where the original source was a press release or a real-time data feed, I have reconstructed the citation based on what a reader would need to locate the information.

Jerven, M. (2013). Poor numbers: How we are misled by African development statistics and what to do about it. Cornell University Press.

Global Financial Integrity. (2020). Illicit financial flows from Africa: 1980–2018. Global Financial Integrity.

United Nations Conference on Trade and Development. (2025). Economic development in Africa report 2025: Tackling illicit financial flows for sustainable development in Africa (UNCTAD/ALDC/AFRICA/2025). United Nations.

Global Financial Integrity. (2023). Trade misinvoicing in 135 developing countries: 2013–2022. Global Financial Integrity.

Orano. (2025, March). 2024 annual results [Press release]. Orano Group. https://www.orano.group

Reuters. (2025, January 20). Niger junta claims French firm Orano pocketed 86% of uranium revenues over 50 years. Reuters. https://www.reuters.com

UxC. (2024). UxC weekly spot price, October 2024. UxC, LLC. https://www.uxc.com

Survie. (2021). Eramet au Sénégal: une mine d’or pour la France, une misère pour le pays [Eramet in Senegal: A gold mine for France, misery for the country]. Survie.

International Monetary Fund. (2021). Tax avoidance in sub-Saharan Africa’s mining sector (IMF Working Paper No. 2021/037). International Monetary Fund.

Reuters. (2024, March 5). Central African states’ central bank pays out record interest on pooled reserves. Reuters. https://www.reuters.com

Nachega, J.-C., & Ndung’u, N. (2001). The CFA franc devaluation and output growth in the CFA franc zone (IMF Working Paper No. 01/141). International Monetary Fund.

France24. (2019, December 21). West Africa’s CFA franc reform: A break with the past? France24. https://www.france24.com

Reuters. (2025, November 10). French parliament ratifies end to role in West African CFA franc. Reuters. https://www.reuters.com

Jeune Afrique. (2020, November 18). Les accords de défense secrets entre la France et ses anciennes colonies d’Afrique [The secret defense agreements between France and its former African colonies]. Jeune Afrique. https://www.jeuneafrique.com

Organisation for Economic Co-operation and Development. (2023). Development co-operation profiles 2023: France. OECD Publishing. https://doi.org/10.1787/aa7e3298-en

RFI. (2024, November 15). French development aid cut by €2 billion in 2025 budget. RFI. https://www.rfi.fr

French Ministry of Economy, Finance, and Industrial and Digital Sovereignty. (2025). French foreign direct investment in Africa reaches €68 billion in 2024 [Press release]. Direction Générale du Trésor.

African Union. (2025). Declaration of the 38th Ordinary Session of the Assembly of Heads of State and Government on the theme of the year: “Year of Justice for Africans and People of African Descent through Reparations”. African Union.