From a few containers in a car park to gigawatt-hours of grid-connected storage: repurposed EV batteries are becoming a quiet force in the energy transition.

IN A DUSTY corner of a Nevada industrial park sits the world's largest collection of used electric-vehicle batteries turned into a working power plant. The system, built by Redwood Materials, can deliver 12 megawatts of power and store 63 megawatt-hours of energy—enough to supply a small town during a grid outage. Every cell inside it once pushed a Tesla, a Nissan Leaf, or a Ford Mustang Mach‑E down a highway. Now, wired together in stationary racks, they charge and discharge in rhythm with the electricity market, arbitraging between cheap midday solar and expensive evening peak power.

This is the second-life battery economy moving from experiment to infrastructure. And it is growing fast.

From pilots to portfolios

The early second-life projects were small and tentative: a handful of Leaf packs behind a fence at a Nissan dealer, a shipping container of modules powering a streetlight. Today the scale is shifting by orders of magnitude. Redwood Materials alone now receives more than 20 gigawatt-hours of end‑of‑life batteries each year, mostly from automotive trade‑ins and production scrap. Many of the packs that arrive still carry 50% or more of their original capacity. Straubel's engineers test, grade and reassemble the best of them into grid‑ready storage blocks that cost, the company says, "substantially less" than equivalent new systems.

The economics are attracting serious industrial customers. Rivian, the electric-truck maker, has partnered with Redwood to turn more than 100 of its own retired packs into a 10 MWh dispatchable storage installation at its Illinois manufacturing plant. The batteries, born on the same assembly line they now help power, buffer the factory's energy demand and shave peak charges from the local utility. It is a closed‑loop demonstration that makes both environmental and financial sense.

B2U Storage Solutions, a California‑based operator, has gone further into grid‑scale territory. In West Texas, the company has connected 500 retired EV packs—mostly from Nissan Leafs and Honda Claritys—into a 24 MWh system that trades in the ERCOT wholesale market. The packs, still wearing their original automotive casings, sit on racks under the sun, their state‑of‑health managed individually by proprietary software. B2U claims the batteries can operate profitably for another eight years beyond their automotive retirement.

In Europe, Nissan has been quietly building a portfolio of second‑life installations. The Spanish enclave of Melilla, a grid‑island on the north African coast, now relies on 48 used Leaf packs combined with 30 new ones to provide 4 MW of backup power for its 90,000 residents. At Rome's Fiumicino Airport, 84 Leaf packs form a 2.1 MWh battery energy storage system that smooths terminal demand and provides emergency backup—a validation at one of the world's most security‑conscious locations. In the port of Vigo, just 12 Leaf packs (30 kWh each) buffer an ultra‑fast charging station, absorbing grid spikes and delivering power at rates the local network could not otherwise support.

A Finnish start‑up, Cactos, has taken a modular approach, repackaging Tesla Model S packs into 100 kWh "Cactos One" units that sit in commercial basements, providing peak‑shaving and backup for hotels and offices. The business model is simple: the used packs are cheap enough to undercut new lithium‑ion storage, and their residual capacity is perfectly matched to the shallow cycling of daily demand management.

How big is the market?

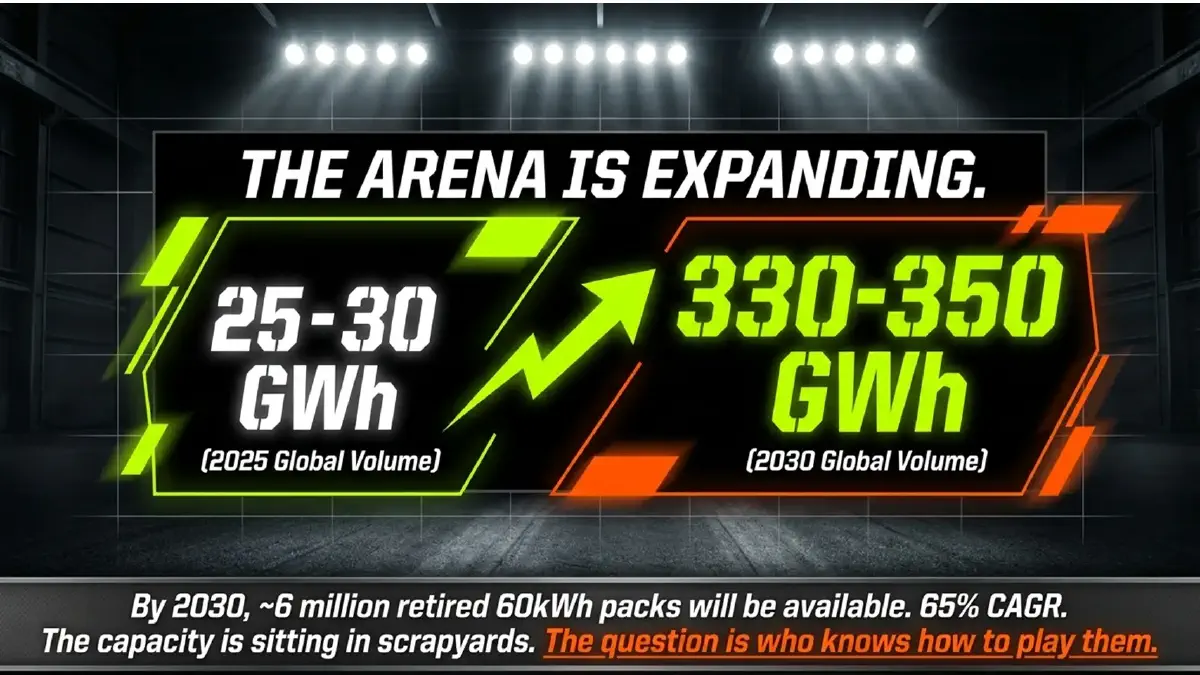

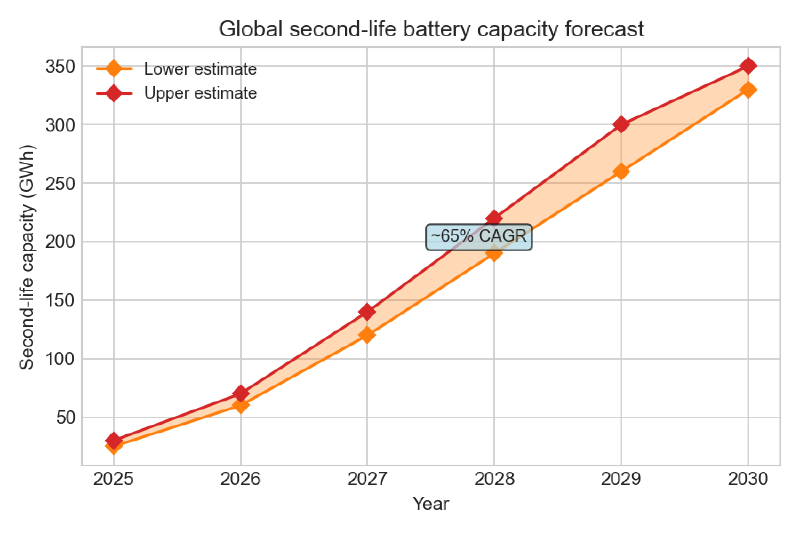

The numbers are starting to add up. In 2025, analysts estimate that 25‑30 gigawatt‑hours of second‑life battery capacity will be deployed globally, primarily in stationary storage. By 2030, that figure is projected to reach 330‑350 GWh—equivalent to roughly 5‑6 million retired 60 kWh packs repurposed into grid assets. The compound annual growth rate of roughly 65% reflects both the rising tide of EV retirements and the falling cost of the power electronics needed to integrate used batteries into standard storage architectures.

[FIGURE: Global second-life battery capacity forecast, 2025-2030]

What makes a pack worth repurposing?

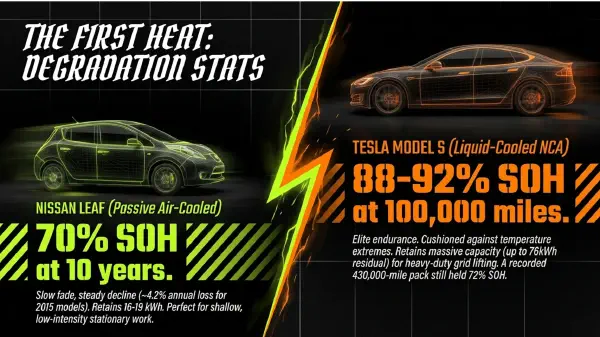

Not all retired batteries are equal. The viability of a second‑life project depends on an intricate calculus: the pack's remaining capacity, its internal resistance, the rate at which it continues to degrade, and the cost of disassembly, testing and reassembly. A liquid‑cooled Tesla pack that has led a gentle life in a cool climate may slide into stationary service with minimal re‑engineering. A passively‑cooled Leaf pack that spent a decade baking in Arizona sun may be barely worth the trucking cost.

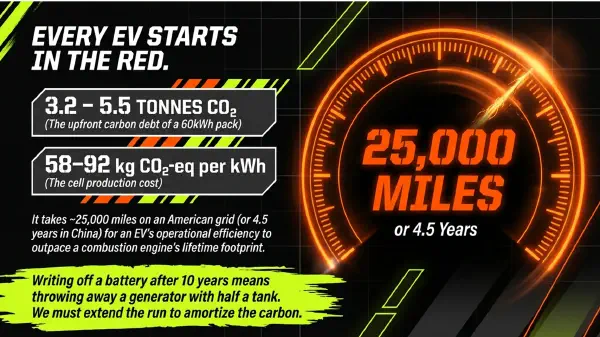

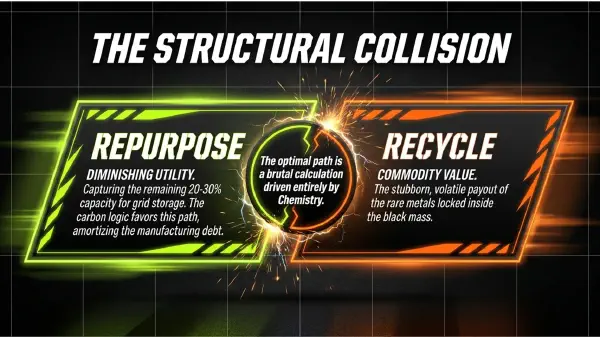

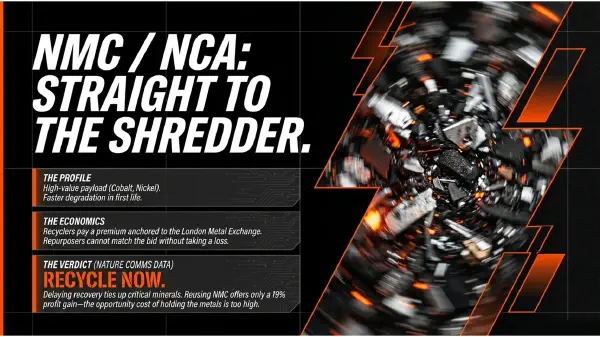

Chemistry matters enormously. Lithium‑iron‑phosphate (LFP) packs, which are rapidly becoming the dominant automotive chemistry, degrade slowly, tolerate thousands of deep cycles, and contain little valuable metal to recycle. That makes them prime candidates for second‑life repurposing: they have more to give and less to lose. Nickel‑rich chemistries (NMC, NCA) degrade faster and contain high‑value cobalt and nickel that make immediate recycling attractive. The economic scales tip differently for each.

And labour remains the stubborn cost. A pack must be carefully discharged, opened, tested, sometimes disassembled to the module level, and fitted with a new battery management system. Carnegie Mellon University and the US National Renewable Energy Laboratory estimate that testing and grading alone costs around $14 per kWh at the pack level, rising to $29 per kWh if modules must be extracted. Building a complete second‑life battery storage system—with inverter, enclosure and thermal management—adds another $127‑144 per kWh. At current new‑battery prices, that leaves a narrowing margin.

Yet the market is finding its equilibrium. As the pipeline of retired packs swells from thousands to millions, the infrastructure for grading, logistics and reassembly is maturing. The next challenge is what happens when the second life ends—and whether the materials inside can be recovered to seed a third.

Next: Recycling—the 99% promise and its limits.