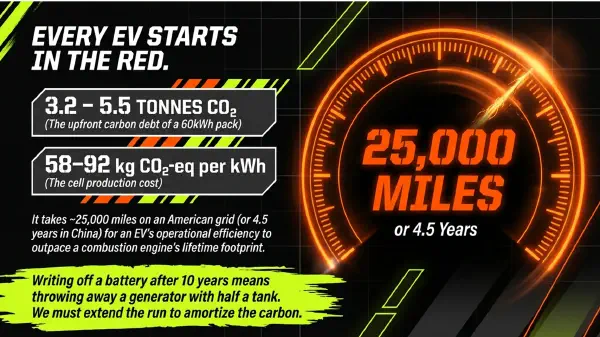

Chinese recyclers boast near‑perfect recovery of battery metals. European regulators are setting binding targets. But the last few percent are the hardest—and most expensive—to capture.

THE DREAM of a circular battery economy is seductively simple. An electric car reaches the end of its road life, its tired pack is collected, and the valuable metals inside—nickel, cobalt, lithium, copper—are extracted and fed back into new cells, reducing the need for mining and slashing the carbon footprint of every future vehicle. In Chinese industrial parks, that dream already looks remarkably close to reality.

Chinese recyclers, led by CATL’s subsidiary Brunp and state‑owned operators in Tianjin, claim to recover 99.6% of the nickel, cobalt and manganese from spent lithium‑ion batteries, and 96.5% of the lithium. Those are extraordinary numbers, achieved through hydrometallurgical processes that dissolve the crushed battery material—known as “black mass”—in acid baths and then precipitate out the target metals one by one. The plants operate at a scale that Western competitors can only envy: Brunp alone now handles more than half of China’s domestic battery recycling volume.

The regulatory race

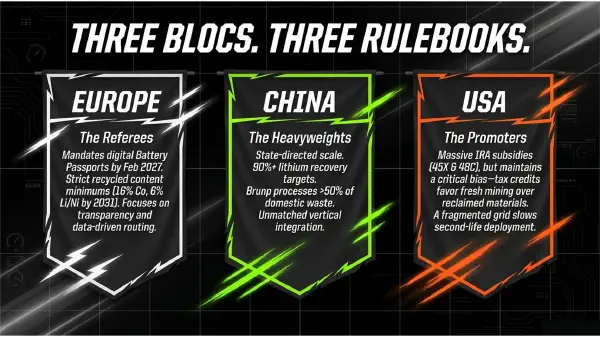

Europe, determined not to lose the circular‑economy race, has written binding recovery targets into its new Battery Regulation. By 2027, recyclers must hit 90% recovery for cobalt, nickel and copper, and 50% for lithium. By 2031, the bar rises to 95% for the three high‑value metals and 80% for lithium. These are not aspirations; they are legal requirements, backed by penalties and linked to the digital Battery Passport that every pack sold in the EU must carry from February 2027.

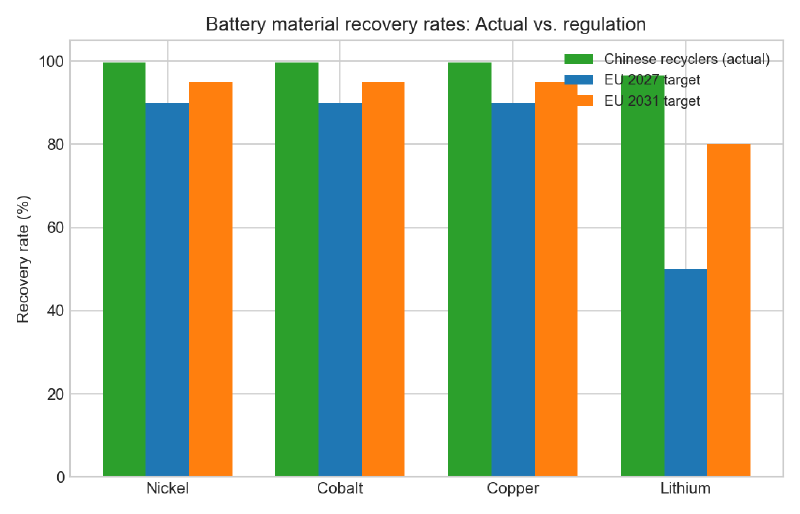

[FIGURE: Battery material recovery rates – Chinese recyclers vs EU regulatory targets]

The chart tells a story of a narrowing gap. Chinese industry already comfortably exceeds the EU’s 2031 targets for nickel, cobalt and copper, and is within striking distance on lithium. But the distance between 96.5% and 80% is not merely arithmetic; it is a measure of the chemical difficulty of extracting lithium from complex cathode structures without destroying the graphite anode or generating toxic fluorine compounds. Every additional percentage point of recovery costs more energy and more reagent—and emits more CO₂.

The direct‑recycling shortcut

A cleaner alternative is emerging from university laboratories and a handful of start‑ups. “Direct recycling” preserves the cathode crystal structure rather than dissolving it, allowing the recovered material to be re‑lithiated and inserted into new cells with far less energy. Lifecycle assessments suggest this pathway generates just 0.6‑8.1 kg of CO₂ per kilogram of recovered cathode material, compared with the heavy chemical footprint of conventional hydrometallurgy. Its energy cost is a fraction of the competition’s, and the economic cost, at $0.9‑4.1 per kilogram, looks compelling.

But direct recycling is extraordinarily fussy. It requires a pure stream of a single cathode chemistry, meaning packs must be sorted meticulously—not an easy task when the end‑of‑life feedstock is a jumble of NMC, NCA and LFP chemistries from different decades and manufacturers. Scaling direct recycling from a laboratory curiosity to an industrial process remains one of the hardest problems in battery science.

The carbon prize

What is at stake becomes clear when the numbers are run. When a new battery incorporates 95% recycled material, its production carbon footprint can fall by roughly 80%. That would bring the EV‑vs‑ICE break‑even point down to around 15,000 miles—half the current distance—making the climate case for electrification almost unassailable. It is a tantalising prospect, but one that depends on the recycling industry not only hitting the EU’s 2031 targets but surpassing them, and doing so at industrial scale.

The global recycling market is expanding rapidly to meet the opportunity. It was worth an estimated $3.88 billion in 2025, a figure that is projected to more than quadruple to $15.58 billion by 2030, a compound annual growth rate of around 32%. Much of the growth will be in China, but Europe and North America are building capacity fast, spurred by industrial policy and the sheer volume of batteries now approaching end‑of‑life.

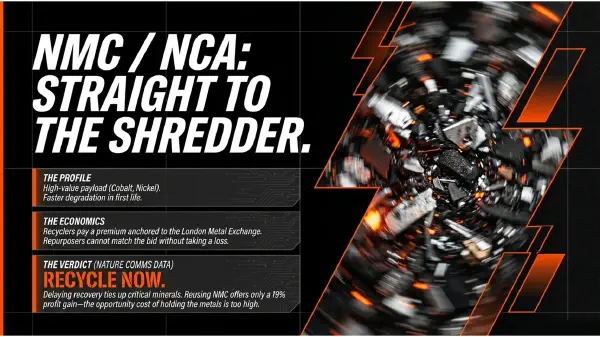

The LFP problem

Yet the recycling industry faces a structural headwind that is quietly reshaping the economics: the rise of lithium‑iron‑phosphate (LFP) chemistry. LFP cells contain no cobalt and no nickel, and the lithium inside them is worth less than the cost of its extraction. For recyclers, that makes LFP an unappealing feedstock. A tonne of spent LFP black mass commands a fraction of the price of an equivalent tonne of NMC—and, in some market conditions, recyclers are effectively being asked to accept it for free or even to charge a gate fee.

This does not mean LFP batteries will be landfilled; the materials can be recovered, and processes are improving. But it does reorder the logic of the battery’s end‑of‑life journey. If recycling an LFP pack loses money while repurposing it can earn a modest return, the market will choose repurposing every time. The chemistry that is most benign for second‑life applications is, almost perversely, the least attractive for recycling.

That is the crux of the structural‑economics problem. The decision between repurposing and recycling is not a binary moral choice but an equation in which cathode chemistry, residual health, labour cost and commodity prices all pull in different directions. The next article examines that equation in detail.

Next: The structural economics—under what conditions does repurposing create more value than immediate recycling?