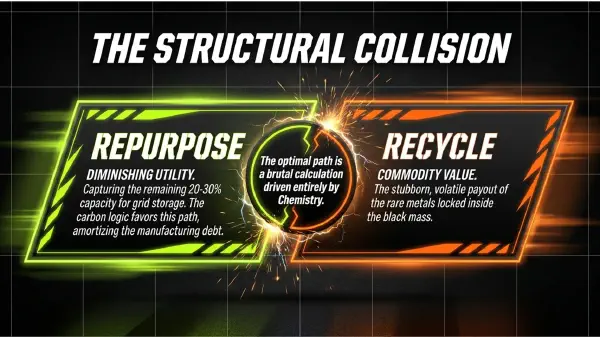

The decision to repurpose or recycle is not a moral one. It is a matter of chemistry, degradation curves and the brutal logic of cash flows.

A RETIRED electric-vehicle battery sits on a pallet in a logistics yard, its state-of-health flickering somewhere between 70% and 80%. The owner faces a choice: sell it to a recycler who will shred it and recover the nickel, cobalt and lithium inside, or send it to a repurposer who will test, reassemble and install it in a stationary storage unit. At that moment, the battery ceases to be an environmental object and becomes an economic one. The right answer depends on which pathway leaves the owner with more cash—and the planet with less carbon.

For years, the debate has been framed as a moral hierarchy: reuse is virtuous, recycling is a last resort. The data now arriving from the first generation of mass-market electric cars show that this framing is too simple. The structural economics of end-of-life batteries are driven by two forces that pull in opposite directions: the diminishing usefulness of the cell as it ages, and the stubbornly high value of the metals locked inside. Which force wins depends, above all, on the cathode chemistry.

The cost of giving a battery a second life

Repurposing a used EV pack is not free. The battery must be carefully discharged to a safe voltage, stripped of its automotive casing, and put through a battery of tests to determine its remaining capacity, internal resistance and propensity to self-discharge. Cells or modules that have degraded unevenly must be identified and sometimes discarded. The surviving components then need a new battery management system (BMS), an inverter, a thermal management solution and a weatherproof enclosure—essentially everything that makes a stationary storage unit except the lithium-ion cells themselves.

Researchers at Carnegie Mellon University and the US National Renewable Energy Laboratory have put numbers on each of these steps. Testing and grading alone costs roughly $14 per kilowatt-hour of nameplate capacity if done at the pack level, rising to $29 per kWh if modules must be extracted and tested individually. Building a complete second-life battery energy storage system (SL‑BESS)—with power electronics, cabinets, cooling and fire suppression—adds another $127–144 per kWh. All in, the repurposing premium over and above the bare used cells can reach $160 per kWh.

That leaves a narrowing window. New lithium-iron-phosphate (LFP) battery packs are now being quoted at $85–95 per kWh at the cell level from Chinese producers. A repurposed storage unit, even if the used cells are free, must compete against that benchmark. When the price of new cells drops faster than the cost of the labour needed to refurbish old ones, the second-life proposition gets squeezed. And that is precisely what has been happening.

The richness of the scrap pile

The alternative route—immediate recycling—is buoyed by the very metals that make automotive batteries expensive in the first place. Nickel and cobalt command high and volatile prices on global commodity markets. Lithium, though cheaper per tonne, is increasingly in demand. A tonne of NMC (nickel-manganese-cobalt) black mass—the crushed and sieved residue of shredded batteries—can be worth several thousand dollars, depending on spot metal prices and the purity of the feedstock.

For an NMC pack, the recycling revenue often exceeds the cost of collection, transport and processing. Hydrometallurgical plants in China, such as those operated by CATL’s Brunp subsidiary, extract 99.6% of the nickel, cobalt and manganese and 96.5% of the lithium, delivering a clean profit to the recycler and, typically, a positive scrap value to the battery owner. In effect, an NMC battery at end of life is a valuable pile of ore in a convenient rectangular housing.

LFP batteries are another matter entirely. They contain no cobalt, no nickel, and only a modest amount of lithium—perhaps 1-2% by weight—that is chemically tedious to recover. The scrap value of an LFP pack is close to zero, and in some markets recyclers demand a gate fee to accept it. If a battery is made of LFP, its owner has no financial incentive to recycle it, and every incentive to find a second life that can generate a revenue stream instead.

The Nature verdict: repurpose first, but only for the right chemistry

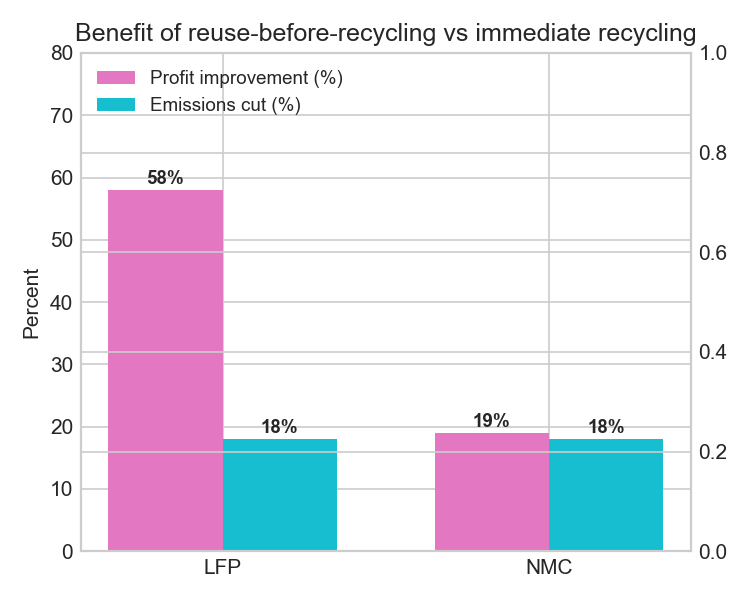

The sharpest analysis yet of this trade-off was published in Nature Communications in 2024. A team of researchers modelled the full lifecycle—first use in a vehicle, potential second use in stationary storage, and eventual recycling—for both LFP and NMC chemistries. They compared the “reuse-before-recycling” pathway with the “immediate recycling” pathway on two dimensions: profitability and carbon emissions.

The results were striking—and asymmetric. For LFP batteries, reuse-before-recycling improved profit by 58% and cut emissions by 18% compared with shredding the pack straight away. The gain came from the extra years of grid service, which displaced fossil-fuel generation and generated revenues that comfortably exceeded the repurposing costs. For NMC batteries, the same pathway improved profit by just 19%, and the emissions reduction was also 18%. The difference in profit reflected the high opportunity cost of delaying recycling: an NMC pack that is put into second life ties up valuable metals that could have been sold immediately on strong commodity markets.

[FIGURE: Profit improvement and emissions cut from reuse-before-recycling vs. immediate recycling for LFP and NMC batteries]

What the market will pay

These findings are already shaping commercial behaviour. Repurposers bidding for end-of-life battery packs from scrapyards and vehicle dismantlers are pricing according to chemistry and condition. For a used LFP pack with verified gentle history and high residual capacity, repurposers are willing to pay between $3 and $70 per kWh of nameplate capacity—a wide range that reflects the difficulty of assessing remaining life without expensive testing. For an NMC pack, the bid is often zero or negative from repurposers, because the recycler’s offer—anchored to the London Metal Exchange cobalt price—sets a floor that the repurposer cannot match.

A fair-value model developed by researchers at the University of Mannheim and Stanford University formalises this logic. LFP batteries are “consistently suitable” for second life, the authors conclude, because their degradation is slow, their cycle life is long, and the alternative—recycling—yields almost no financial return. NCX batteries (the family that includes NMC and NCA) are generally better off being recycled immediately unless the pack has enjoyed an unusually gentle first life and can serve a high-revenue second application, such as frequency regulation in a premium electricity market.

The logic is in the chemistry

The structural economics boil down to a simple truth: a battery’s value at end of automotive life is the higher of two numbers—the net present value of a future stream of stationary-storage revenues, minus the cost of repurposing, and the net scrap value of its materials, minus the cost of recycling. For LFP, the second number is close to zero and the first is modestly positive, so repurposing wins almost every time. For NMC, the second number is buoyant and the first is uncertain, so recycling wins more often than not.

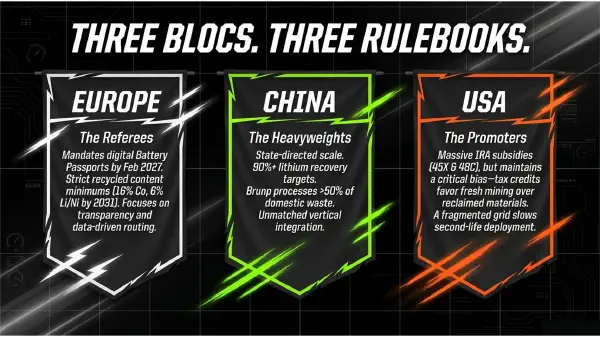

That has profound implications for policy. A single, rigid waste‑management hierarchy—reuse before recycle, in all cases—would misallocate capital, forcing NMC packs into low‑value second lives at the expense of rapid recovery of critical minerals. A smarter approach, already being explored in the EU Battery Regulation’s digital passport, is to embed battery‑chemistry data and first‑life usage history into the pack’s identity, so that the end‑of‑life routing decision can be made on an economic basis, pack by pack, not by blanket rule.

The market is moving faster than the regulators. Repurposers are specialising in LFP; recyclers are salivating at the coming wave of NMC retirements. Both will have plenty of feedstock. The challenge for the industry—and for the climate—is to ensure that each battery takes the path that extracts the most value and the least carbon, in the right order.

Next: The policy architecture—how the EU, China and America are shaping the repurpose‑versus‑recycle decision.