Three blocs, three approaches—and a decision about repurposing versus recycling that is being shaped as much by regulation as by market forces.

THE RETIRED battery sitting on its pallet does not exist in a policy vacuum. Its fate—whether it is routed to a second‑life energy‑storage unit or sent directly to the shredder—is increasingly determined by a web of regulations, incentives and targets stretching from Brussels to Beijing to Washington. The three great economic powers have each taken a different approach to the problem of battery end‑of‑life, and those choices are already reshaping the flow of used packs around the world.

The European Union is building the most prescriptive architecture, one that demands transparency and recycled content and, in effect, forces a conversation between the battery’s first and second lives. China is wielding state‑directed industrial policy to dominate the recycling industry and secure strategic minerals. And America, for all the ambition of the Inflation Reduction Act, has yet to resolve a regulatory bias that favours mining fresh minerals over reclaiming spent ones.

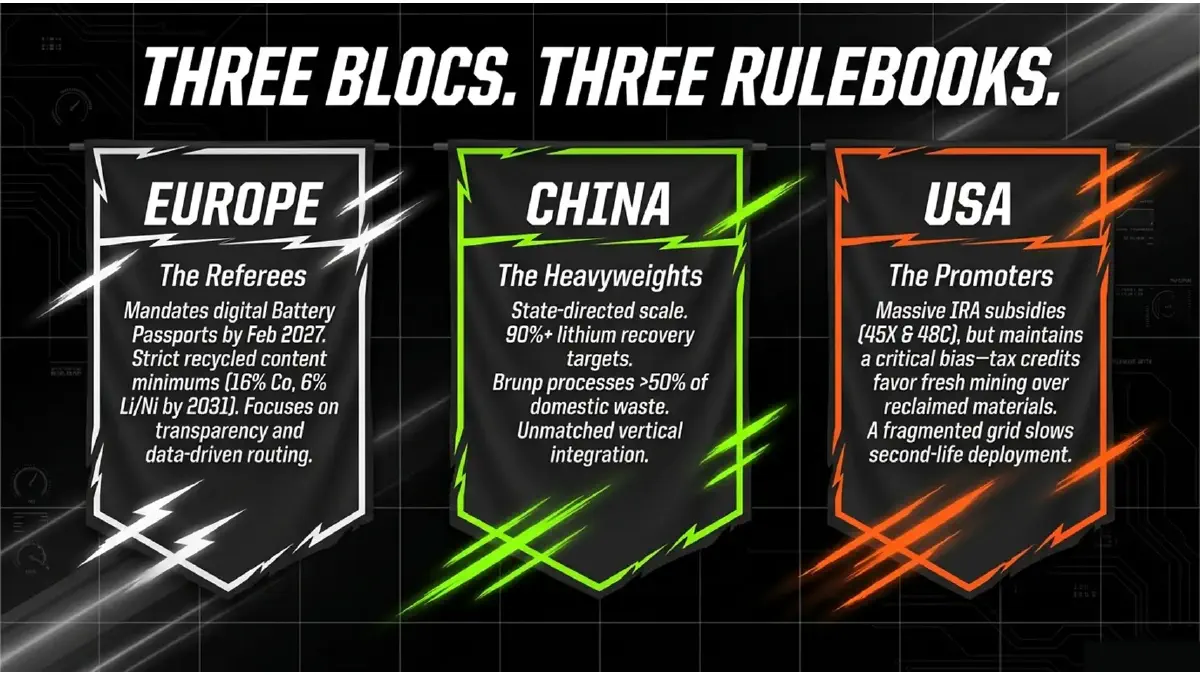

Europe: the passport and the mandate

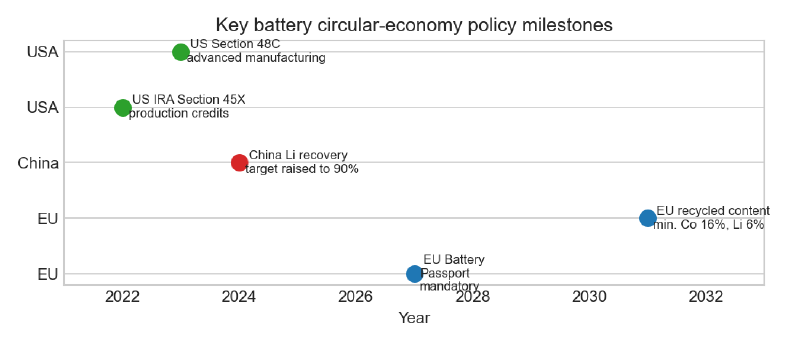

At the heart of the EU’s Battery Regulation, which entered into force in 2023 with staggered compliance deadlines, is the digital Battery Passport. From February 2027, every electric‑vehicle and industrial battery sold in the bloc must carry a digital record that documents its carbon footprint, its recycled‑content share and its supply‑chain due‑diligence history. For the first time, a battery’s entire identity—from the mine to the scrapyard—will be machine‑readable and legally auditable.

For the second‑life industry, the passport is a quiet revolution. A repurposer receiving a pallet of aged Leaf or Model S packs will be able to scan a QR code and retrieve the pack’s original chemistry, its first‑life usage history, its current state‑of‑health as recorded by the vehicle’s BMS, and the carbon cost already sunk into its manufacture. That eliminates much of the expensive testing and guesswork that currently constrains the market. It also makes the repurpose‑or‑recycle decision an informed one, pack by pack, rather than a gamble.

The regulation does not stop at information. By 2031, new batteries must contain minimum shares of recycled material: 16% cobalt, 6% lithium and 6% nickel. Those numbers will rise over time. The effect is to create a guaranteed pull‑demand for recycled battery metals, shoring up the economics of recycling even when virgin commodity prices are low. For NMC packs rich in cobalt and nickel, that makes the recycling route more attractive, pulling against the logic that might otherwise favour a second life.

But the EU is not attempting to pick a winner between repurposing and recycling. The passport enables the market to decide case by case, while the recycled‑content mandate ensures that when a pack does finally reach the shredder, its materials will find a home. It is an elegant piece of regulatory engineering—provided the passport data are reliable and the enforcement is credible.

China: the recycling superpower

China’s approach is less about consumer transparency and more about strategic control of critical minerals. The country has few domestic sources of cobalt and high‑grade nickel, but it has the world’s largest fleet of electric vehicles and is therefore sitting on an enormous future mine of battery metals. The government’s policy goal is simple: ensure that as much of that material as possible is recovered, processed and fed back into domestic battery manufacturing, reducing reliance on imports from the Democratic Republic of Congo and Indonesia.

A series of national standards governs battery dismantling and recycling, and the Ministry of Industry and Information Technology (MIIT) has progressively raised recovery targets. In 2024, it increased the lithium recovery requirement from 85% to 90%, a signal that it expects the industry to push closer to the 96.5% already claimed by the largest players. CATL’s subsidiary Brunp now handles more than half of China’s domestic battery recycling, enjoying a mix of scale, state support and vertical integration that makes it the most formidable recycler on the planet.

China’s policy framework is less explicit about second‑life repurposing, but it indirectly encourages it for LFP chemistries, which dominate the domestic market. Since LFP packs hold little value for recyclers, a second life in grid‑connected or behind‑the‑meter storage is often the only economically rational pathway. Provincial governments and state‑grid operators have funded pilot projects that repurpose retired EV packs into community storage, particularly in rural areas. The combination of state‑subsidised collection networks and a cost‑sensitive domestic storage market is quietly building the world’s largest second‑life capacity.

America: credits, gaps and the mine‑versus‑reclaim bias

The United States has unleashed the most generous battery‑manufacturing subsidies in the world through the Inflation Reduction Act of 2022. Section 45X provides production tax credits for battery cells and for the critical minerals used in them. But the credits, as originally written, make no distinction between minerals freshly mined and those recovered from recycling. The result, critics argue, is a system that effectively subsidises mining more heavily than reclaiming, because mining operations can more easily structure themselves to claim the full credit value.

Section 48C of the IRA offers investment tax credits for advanced manufacturing projects, including battery recycling facilities. Several large recyclers, including Redwood Materials and Li‑Cycle, have used these credits to support plant construction. Yet the absence of a federal recycled‑content mandate—of the kind the EU has adopted—means there is no demand‑side pull for the materials those plants will produce. The economics of American recycling remain heavily dependent on the commodity cycle and the willingness of battery manufacturers to accept recycled feedstock.

The US has also been slow to develop a federal framework for second‑life storage. Safety standards, permitting rules and grid‑interconnection protocols for repurposed batteries remain a patchwork of state‑level interpretations. This vacuum creates uncertainty for developers, who cannot be sure that a second‑life system approved in Texas will be accepted in California. The result is a market that is growing—Redwood’s Nevada microgrid and B2U’s Texas plant are proof of that—but far more slowly than its potential suggests.

[FIGURE: Key battery circular-economy policy milestones by region]

Who gets it right?

The three models reflect different political and economic imperatives. Europe, with its scarce raw materials and strong environmental lobbies, is betting on regulation to create a transparent, circular market that extracts maximum value from each battery. China is treating battery waste as a strategic resource, deploying state muscle to capture the entire value chain. America is relying on subsidies to build capacity but has not yet completed the regulatory architecture needed to make the market self‑sustaining.

For the battery industry, the message is clear. Any company handling end‑of‑life packs will need to navigate three distinct regulatory environments, each with its own incentives, targets and administrative requirements. The winners will be those who build the data systems—the digital passports, the testing protocols, the traceability platforms—that can satisfy all three, turning regulatory complexity into a competitive advantage.

The policy landscape, like the batteries themselves, is still taking shape. But the direction of travel is unmistakable: the idle battery on a pallet is being drawn into a web of rules that will decide whether it gets a second life, and what happens when that second life is over.

Next: Case studies that prove the model—from Fiumicino Airport to the Texas grid, the real‑world projects demonstrating what second‑life batteries can do.