As wave two of EV retirements arrives, a collision between cheap new batteries and rising second-life capacity will determine whether repurposing flourishes—or gets crushed.

IN 2026, more than 100,000 electric vehicles will be scrapped in the United States alone. That is the first ripple of a tsunami. By the end of the decade, the annual retirement figure will have tripled, and the global stock of end‑of‑life EV batteries will be measured not in thousands of packs but in millions. The pipeline of potential second‑life capacity is swelling from roughly one gigawatt‑hour today—barely a rounding error in the global electricity system—to a projected 330–350 GWh by 2030. That is more than all the grid‑scale battery storage installed worldwide at the start of 2025. The question is not whether the feedstock will exist; it is whether anyone will be able to make money from it.

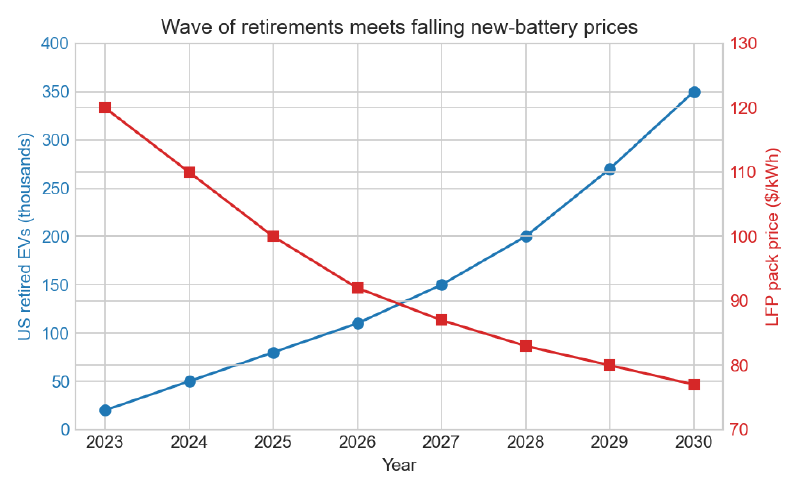

[FIGURE: US retired EVs versus new LFP battery price, 2023–2030]

The figure captures the tension at the heart of the second‑life industry’s future. The blue line—the number of EVs reaching the scrapyard each year—climbs relentlessly. The red line—the price of a new lithium‑iron‑phosphate (LFP) battery pack, the benchmark against which all stationary storage is measured—falls just as steadily, from around $120 per kWh in 2023 to an expected $77 per kWh by 2030. These two lines are heading in opposite directions, and the space between them is where second‑life batteries must carve out a living.

The LFP wave

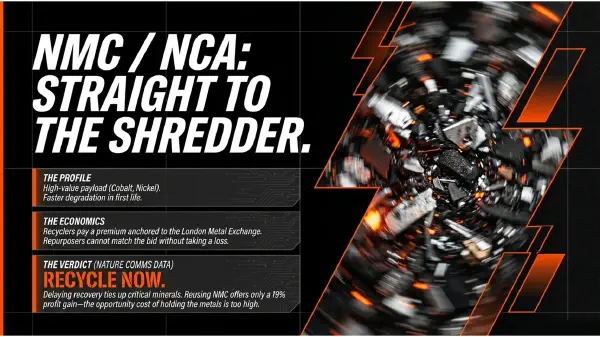

The chemistry of the retirement stream is about to flip. The first generation of mass‑market EVs were overwhelmingly nickel‑rich: NMC and NCA packs loaded with cobalt that made them worth more dead than alive in a stationary storage rack. But the global industry is pivoting fast to LFP, which contains no cobalt, little nickel and just enough lithium to be a nuisance to recover. LFP’s share of the global EV battery market passed 40% in 2024 and is still rising. By 2028, the majority of batteries reaching end‑of‑life will be LFP.

In one sense, this is a gift to the second‑life industry. LFP packs degrade slowly, tolerate thousands of deep cycles and have virtually no scrap value to compete with the revenue from a second life. They are, as the Nature Communications analysis showed, the chemistry for which repurposing makes unambiguously more sense than immediate recycling. In another sense, however, the LFP wave presents an existential problem: it is precisely this chemistry that is driving the collapse in new‑battery prices. If a brand‑new LFP cell costs $50 per kWh at the factory gate and a fully packaged stationary storage system can be built for under $100 per kWh, then a used pack—degraded by 20%, requiring expensive testing, disassembly and reassembly—must be acquired for next to nothing to remain competitive.

The automation imperative

The bottleneck is labour. Testing, grading and reassembling a used pack currently costs between $14 and $29 per kWh for the battery alone, plus a further $127–144 per kWh to integrate it into a weatherproof, grid‑ready enclosure. That total of roughly $160 per kWh is viable only when the alternative—a new storage system—costs substantially more. As new‑system prices dip toward the same level, the repurposing premium becomes untenable unless the labour component can be slashed.

That is why the most important technology in the second‑life industry may not be battery chemistry or power electronics, but robotics. Automated disassembly lines that can safely discharge a pack, open its casing, extract and test modules, and reassemble them into new configurations without human hands are now being prototyped in European and Chinese research labs. If they succeed, the testing‑and‑grading cost could fall by an order of magnitude. If they fail—or arrive too late—the window for profitable repurposing will narrow to a sliver of niche applications.

Redwood’s ambition and the market’s verdict

Redwood Materials, the industry bellwether, is betting that the automation curve will bend in its favour. The company already receives more than 20 GWh of end‑of‑life batteries each year and expects to deploy at least 5 GWh annually of additional second‑life capacity as the retirement wave builds. Its Nevada microgrid is both a profit centre and a laboratory for the processes that will be needed at scale. JB Straubel, the company’s founder, has described the second‑life opportunity as a “race against new battery prices” that his engineers are determined to win.

But the market’s verdict is not yet in. The global second‑life pipeline is forecast to grow at a compound annual rate of around 65%, reaching the 330–350 GWh mark by 2030. Even if that projection proves optimistic—and it depends on the timely arrival of automation, supportive regulation and stable electricity prices—it suggests an industry that will be measured in tens of gigawatt‑hours, not hundreds. That is a substantial business. It is not a replacement for recycling, nor does it need to be.

The end of the sequence

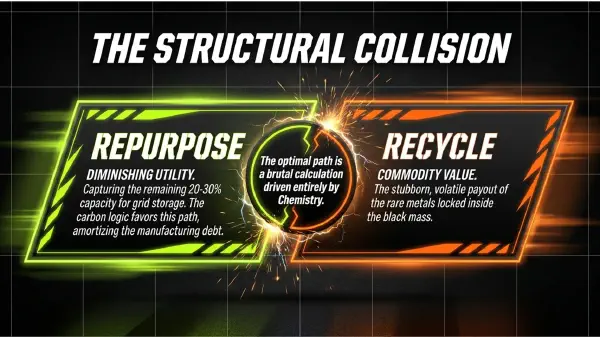

What the data from the first generation of mass‑market EVs have taught us is that the repurpose‑or‑recycle question is a false binary. The optimal pathway is a sequence: extract a second life of energy services from LFP packs, then recycle them when their capacity is genuinely exhausted; recycle NMC packs immediately unless they are unusually healthy and can serve a high‑value application. The digital Battery Passport, arriving in Europe from 2027, will provide the data to make that decision pack by pack, rather than by rule of thumb.

The looming test is whether the economics of that sequence can survive the price collapse in new LFP cells. If used batteries must compete head‑to‑head with new ones on a pure dollar‑per‑kilowatt‑hour basis, many will lose. But if they can be positioned in applications where modest upfront cost, deferred capital expenditure or sustainability credentials matter more than marginal efficiency—peak‑shaving at factories, backup for critical infrastructure, storage for island grids—they will continue to earn their keep.

The carbon logic remains unchanged. Every kilowatt‑hour of renewable energy shifted by a second‑life battery displaces a kilowatt‑hour of fossil generation, amortising the carbon debt of manufacturing over more useful work. The economic logic will depend on whether the industry can cut its costs faster than the price of a new cell can fall. That race is now well under way. The next ten million packs will tell us who wins.

This is the final article in the “Second Life, Second Chance” series on the structural economics of end‑of‑life EV batteries.