In the summer of 1858, two warships—one British, one American—met in the middle of the Atlantic to splice together a copper wire insulated with gutta-percha. Queen Victoria and President James Buchanan exchanged stilted pleasantries over the first transatlantic telegraph cable, a miracle of Victorian engineering that failed within weeks. Yet the dream did not die. By the end of the century, the British Empire had woven a web of submarine cables that it called the “All-Red Line,” a network that connected every continent on earth and passed only through British-controlled territory. When war came in 1914, one of Britain’s first acts was to sever Germany’s undersea links, plunging Berlin into an information blackout from which it never fully recovered. The cables were not just conduits; they were the nervous system of empire, and controlling them meant controlling the world’s conversation.

A century and a half later, the conversation has become a torrent. Submarine fibre-optic cables carry 95% of all intercontinental data—emails, video streams, financial transactions, diplomatic cables, battlefield telemetry. More than $10 trillion in daily financial payments alone travel across these glass threads, lying no thicker than a garden hose on the ocean floor. And the new owners of this nervous system are not empires with navies but a quartet of American technology firms that, in the space of two decades, have gone from being customers of telecoms operators to the dominant force in cable laying, ownership, and control. This is the fourth article in our series on the infrastructure rentiers. It maps the silent capture of the seabed, and asks what happens when the physical backbone of globalisation belongs to a handful of private, foreign-registered monopolies.

From consortia to cloud companies#

For most of the internet’s history, submarine cables were built by clubs of national telecommunications carriers. A consortium of perhaps a dozen companies—France Télécom, Deutsche Telekom, AT&T, NTT, and so on—would pool capital, share capacity, and each own a fraction of the system. The model was slow, consensual, and, crucially, distributed. No single company, and no single country, could command the whole. These cables were subject to national regulations and, in times of crisis, to the foreign-policy objectives of the states where the carriers were domiciled. But the carriers were utilities, not empires, and the ownership structure reflected a multilateral world.

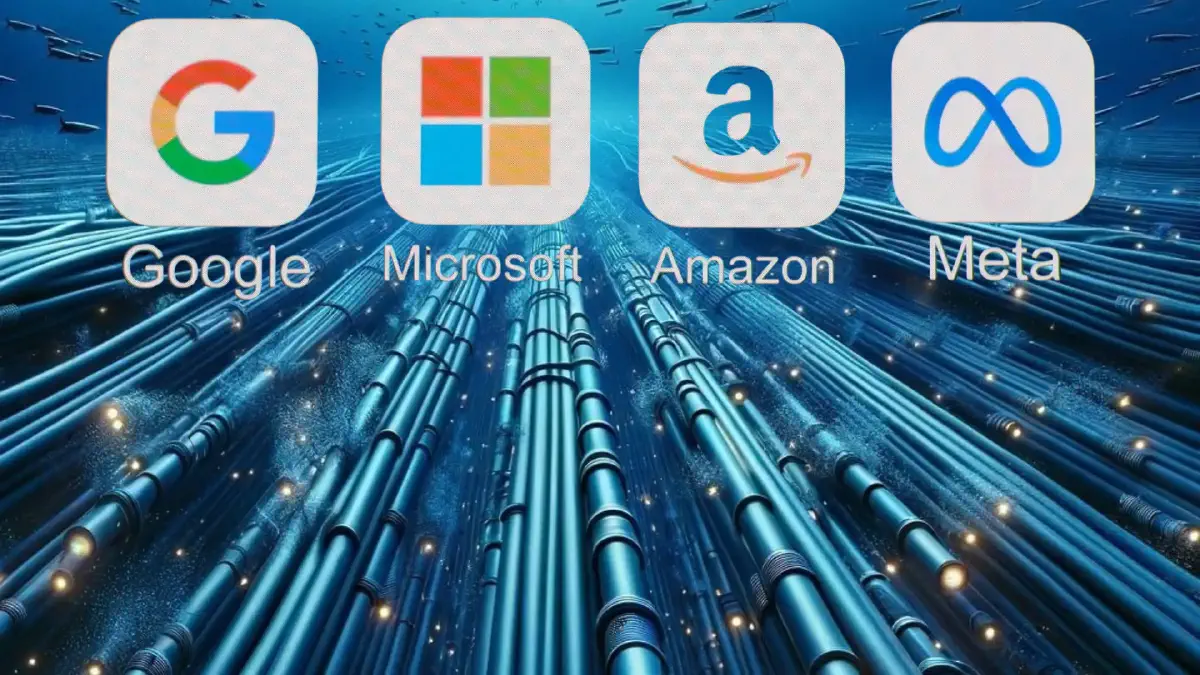

That world has vanished. In its place has risen a hyper-concentrated market in which four American firms—Google, Meta, Microsoft, and Amazon—now control an estimated 71% of global undersea cable capacity. The shift began in the early 2010s, when these companies, then still primarily content providers, started snapping up capacity to link their data centres across oceans. They quickly realised that buying wholesale from telecoms was inefficient. Why pay rent to a consortium when you could lay your own cable, own it entirely, and keep the excess capacity for yourself? And so they began to build.

Google led the charge. It has invested in more than 20 submarine cable systems, including Curie (connecting the United States to Chile), Dunant (crossing the Atlantic), Grace Hopper (linking North America to Europe), and Equiano (running from Portugal to South Africa). Microsoft and Amazon followed, co-investing in multiple transatlantic and transpacific routes. Meta, not to be outdone, is planning Waterworth: a 40,000-kilometre, fully Meta-owned cable that will circle the globe, at an estimated cost of several billion dollars. These are not small projects. They are the digital equivalent of the Suez Canal, built not for national glory but for corporate latency reduction.

The horizontal bar above is as blunt as a gavel. Seventy-one percent of the world’s undersea capacity sits in the hands of four U.S.-headquartered companies. They have become the gatekeepers of the ocean floor, deciding where cables land, who gets access, and at what price. A former TeleGeography analyst describes the situation with a maritime metaphor: “In the 19th century, the Royal Navy charted the sea lanes. Today, Google’s procurement department does.”

The Geography of Control#

To understand the leverage that cable ownership confers, one must appreciate the geography of the network. Submarine cables do not scatter randomly across the seabed. They follow specific, predictable paths, dictated by bathymetry, coastal landing rights, and the imperative to connect major economic hubs. A cable from New York to London, for instance, will almost certainly touch land in Cornwall and Long Island. The same handful of “choke points” recur across the global map: the Luzon Strait between Taiwan and the Philippines, the Bab-el-Mandeb at the southern entrance to the Red Sea, the Florida Strait, the Strait of Malacca. These are the maritime equivalents of the mountain passes of old, and they are increasingly governed not by admiralties but by the capacity‑planning spreadsheets of Big Tech.

Google’s Equiano cable, for example, does not just link Portugal and South Africa; it has landing points in Nigeria, Togo, and Namibia, countries that previously relied on older, slower cables owned by legacy consortia. By introducing massive new bandwidth at lower cost, Google has, in effect, set the connectivity agenda for much of West Africa. Local internet service providers and governments now depend on a cable owned by a single American firm. Should that firm decide—for commercial, regulatory, or geopolitical reasons—to throttle or withdraw service, the impact would be catastrophic. As a Nigerian digital‑policy official told a regional conference, “We used to worry about the Chinese owning our ports. Now we should worry about who owns our cables.”

The concentration of ownership also has implications for surveillance. Any entity that operates a submarine cable landing station—the physical building where the cable comes ashore and connects to terrestrial networks—can, in principle, intercept the data flowing through it. Under U.S. law, the National Security Agency (NSA) and other intelligence agencies have long operated programmes that exploit this access, often with the compelled assistance of the cable owner. When the owner was a consortium of foreign carriers, the legal and diplomatic path to surveillance was complex. When the owner is a U.S. corporation, subject to the Foreign Intelligence Surveillance Act (FISA) and the CLOUD Act, the path is, legally speaking, much smoother. An American tech giant might not want to be seen as an arm of American intelligence, but the law gives it little choice.

The Investment Surge and its Implications#

The scale of capital now pouring into submarine cables is unprecedented. According to TeleGeography, global submarine‑cable investment over the three years to 2027 is projected to reach $13 billion, nearly double the $7 billion or so spent in the previous three‑year period. The surge is driven almost entirely by the hyperscalers, whose appetite for bandwidth is insatiable. Artificial‑intelligence workloads, cloud gaming, high‑definition video streaming—all demand ever‑fatter pipes between continents.

The grouped bars tell a story of acceleration. The doubling of investment is not a cyclical blip; it is a structural shift. The Big Tech firms are not merely adding capacity; they are laying the foundation for a global digital infrastructure that will be proprietary, vertically integrated, and, for all practical purposes, irreplaceable. They are doing so at a speed and with a budget that no government or consortium can match. As one European telecommunications minister lamented privately, “We are still holding committee meetings to discuss a feasibility study, and Google has already laid the cable.”

This investment gap has a self‑reinforcing quality. The more capacity the hyperscalers build, the cheaper their own bandwidth becomes, enabling them to offer cloud services, streaming, and AI products at lower marginal cost. Competitors—both private and public—face a double bind: they must either lease capacity from the very firms they are trying to compete with, or sink billions into infrastructure that will take years to become operational and may already be obsolete by the time it does. The result is a market that tends inexorably towards monopoly.

The CLOUD Act at Sea#

The legal architecture that surrounds submarine cables is, if anything, even murkier than the cloud or space domains. The United Nations Convention on the Law of the Sea (UNCLOS) declares that all states have the right to lay cables on the high seas, but it says little about ownership or jurisdiction when those cables are privately operated. In practice, the law of the landing country governs the cable at each end, and the law of the corporation’s home country governs everything in between. For the transatlantic cables that now carry the bulk of Western financial and government data, that home country is almost always the United States.

The CLOUD Act, which we examined in the context of cloud computing, applies just as forcefully to submarine cables. An American court can order Google to hand over data intercepted on its Equiano cable, even if that data originated in a sovereign African state and is destined for Europe. The company might resist on privacy grounds, but the legal obligation is clear. And because the cables are private property, the company is not obliged to disclose to the affected governments that their data has been seized. This is not hypothetical. In 2013, the Snowden revelations exposed that the NSA had been tapping undersea cables for years, often with the knowledge of the companies that owned them. The outrage that followed prompted some European countries to reconsider their cable‑ownership rules, but little has changed. The cables are more concentrated now than they were then.

The Return of the All-Red Line#

Imperial Britain’s All‑Red Line was a strategic marvel. By ensuring that every telegraph cable linking the empire touched land only on British soil, London guaranteed that its messages could never be intercepted by a foreign power without the Royal Navy knowing. It was the ultimate expression of territorial sovereignty applied to a new technology. Today’s Big Four are, in a curious way, recreating the All‑Red Line for the digital age—not for Queen and Country, but for the demands of their balance sheets.

Google’s cable map looks remarkably like a modern empire’s nervous system: private, redundant, and under a single administrative control. Amazon’s cloud regions are tethered together by cables that it either fully owns or co‑owns with partners who are, more often than not, the same small circle of American tech giants. When a future crisis erupts—a war, a sanctions regime, a cyber‑attack that requires rerouting traffic—the decisions about which cables to keep open and which to throttle will not be made in the Situation Room by elected officials, but in a network operations centre by engineers answering to a corporate vice‑president. The public may never know that a decision was made at all.

The Sovereignty Trap#

Is there any escape? The short answer is that laying a new submarine cable is fantastically expensive and, for a single nation, almost impossible to justify economically. A state‑of‑the‑art transatlantic cable costs upwards of $250 million. A cable linking Europe to Asia can run into the billions. Even if a government were to fund such a project, it would need landing rights in multiple countries, a feat of diplomacy that takes years. And once built, the cable would need to attract traffic from the very Big Tech firms whose dominance it was meant to circumvent—a circular impossibility.

The European Union has begun exploring the idea of “cable sovereignty,” possibly through public‑private partnerships or by mandating that a certain percentage of capacity on new cables be reserved for non‑commercial, governmental use. The EU’s Global Gateway strategy mentions digital connectivity as a priority, and some officials have floated the idea of an EU‑owned “strategic cable reserve.” But the sums are small, the timelines long, and the political will uncertain. Meanwhile, the Big Tech firms are already laying the cables of the 2030s.

A more fundamental problem is that even if a government owns a cable, it still needs the equipment to light it—the specialised lasers, amplifiers, and branching units that are manufactured by a handful of American and Japanese firms. The supply chain for submarine cable technology is almost as concentrated as the cable ownership itself. True sovereignty over the nervous system would require not just owning a fibre pair but mastering the entire industrial ecosystem behind it. That kind of independence is beyond the reach of all but a superpower.

The quiet capture#

The capture of the submarine cable network by a quartet of American firms is perhaps the most consequential and least understood shift in the infrastructure of globalisation. It happened not through conquest but through market logic. The telecoms consortia, under financial pressure, ceded the high‑growth part of the market to the cloud providers. The cloud providers, needing ever‑cheaper bandwidth, built their own cables. Governments, distracted by more visible threats—terrorism, conventional military build‑ups, trade wars—barely noticed. Now they are waking up to find that the physical layer on which their economies float is owned and operated by their own private sector, or, to be more precise, by the private sector of a single foreign nation.

The nervous system of the global economy, once a messy multilateral commons, has become a proprietary network, controlled by a handful of corporate entities that operate under the jurisdiction of the United States. The cables lie silent in the dark of the ocean, but they pulse with the data of states, armies, and markets. In the next article, we will step back and examine what all this means for the state itself: what does it cost a government to lease its own nervous system, and what happens when the landlord asks for more than just rent?